Increasingly the findings from neuroscience are being applied to the world of finance. This is not surprising as neuroscience has plenty to contribute to our understanding of the decision-making process and the financial decisions we make are among the most important. Expanding our understanding of financial decision-making and how to develop a ‘risk mindset’ can help protect organisations against the type of market booms and busts that plague economies around the world.

Improving financial decision-making

Poor financial decision-making can be damaging at both a personal and a professional level – creating stress in the home and insecurity at work.

Unsurprisingly, low financial literacy levels are a major contributing factor to this; but our own understanding of how we make decisions also affects our decision-making.

Most of us believe that we are able to keep our emotions in check; that we are able to put feelings, emotions, and memories to one side and just base our financial decisions on the cold hard data – the numbers.

Neuroscience has shown us that the brain doesn’t work like that. In fact, our emotions play an important role in decision-making. Consider an occasion when you have been resolute in a decision, but been persuaded otherwise after a talk with a friend, colleague, or family member; emotional reasons often force this change of mind.

When this tendency to make emotional decisions is combined with an increasingly complex financial landscape, where the number of choices for financial products and services is mind-boggling, we begin to understand the risks involved.

Financial service companies need to improve the literacy of their customers. In the past there has been a sense that financial organisations have a vested interest in keeping everything vague and complex, unintelligible to all but a few. But the winning organisations of the future will be educators that simplify their products and services for customers, and raise financial literacy levels.

Recent insights from behavioural economics and neuroscience can assist with designing financial products and marketing campaigns that promote better understanding for customers and employees, encouraging better financial advice, and improving the likelihood of a good financial decision being made.

Developing a ‘risk mindset’

Ensuring that the right financial products are sold to the right people, for the right reasons, and that customers fully understand what they are purchasing, requires a ‘risk mindset’.

This is becoming more necessary as financial regulations become tighter around the world, and financial organisations start to repair the image problems they have experienced in recent years.

But it takes more than just paying ‘lip service’ to regulations; it is about bringing real value to the customer experience.

With the aid of neuroscience and a better understanding of the decision-making process, organisations can:

Create a culture where the ‘regulator’ mindset is adopted in a constructive way, using principles that underlie the regulation rather than just blindly following the letter of the law.

Re-design incentive schemes less likely to result in mis-selling

Develop structured processes and a common language that all areas of the organisation can use to focus on the customer

Adapt existing products and services to have a positive impact on the customer experience

Foster collaboration and change between and within traditional organisational ‘silos’

The team at NeuroPower is at the forefront of introducing new approaches to organisational development through the findings of neuroscience. We apply them to all types of businesses, developing high performing teams and enhancing leadership. Find out more at our website:http://www.neuropowergroup.com.

On January 1, 2016, the EU implemented a new bank restructuring directive. The new and stricter rules are aimed at forcing private stock, bond and deposit holders to accept losses before public funds would be used in a bank restructuring. Although all EU countries are affected by these new rules, Italy remains of particular concern due to the number of distressed loans in the country. The Italian banking index is down almost 20% in 2016 due to concerns over nonperforming loans in the country’s banking system and the limited protection that private investors will receive under the new directive.

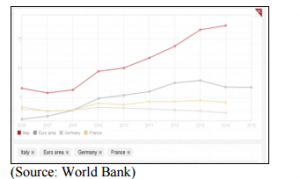

This week, we will look at the overall health of Italy’s banking system as well as the nonperforming loan problem in the country. We will explore the various issues affecting Italy and the EU with regard to finding a solution for Italy’s troubled banking system. Nonperforming Loans Nonperforming loans (NPLs) are loans that debtors are not paying off as agreed upon, but which have not yet been written off by the banks. All countries’ banking systems have some level of NPLs. The chart below shows NPLs as a percentage of total gross loans for various countries. In 2014, Italy’s (red line) ratio stood at 17.3%. The Eurozone average (dark gray line) was 6.8% in the same year and Germany’s ratio was 2.3% (light gray line). By comparison, the U.S. ratio was 1.9% in 2014 (not shown on the chart).

Some sources peg the 2015 level for Italy at 18.0%.

Another measure of NPLs is the ratio of NPLs to GDP. Italy does not have the highest ratio of NPLs to GDP in the Eurozone. In fact, Cyprus, Greece and Ireland all have worse ratios than Italy. However, Italy represents an outsized risk due to its large size. It is the third largest economy in the Eurozone, after Germany and France, and the eighth largest economy worldwide. Thus, while smaller European countries may have worse NPL ratios, the relative size of “bailout” funds for those countries pales in comparison to what would be needed in Italy.

This makes a banking crisis in Italy much more serious than a crisis in any other smaller European country. The BRRD The EU Bank Recovery and Resolution Directive (“BRRD”), which became effective at the beginning of this year, requires that shareholders, bond holders and even large depositors bear the costs of a bank restructuring before government funds will be used to bail out the failing institution. This mechanism is informally called a “bail-in,” with stakeholders providing the funding as opposed to a “bailout” which uses public funding. In the case of a business failure, it is not uncommon to require shareholders to lose money.

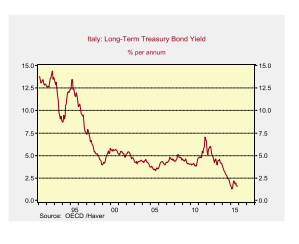

Even certain classes of bond holders usually lose some, if not all, of their investment. The approach, which was first used during the Cyprus bank failures in 2012-2013, will require losses from all subordinated debt holders as well as accounts with balances over €100,000. Smaller deposits would still be excluded from the bail-ins. Background on Italy’s Markets The Italian bond market enjoyed a period of falling yields in anticipation of the euro’s introduction. Financial markets interpreted the euro to mean that all Eurozone countries’ credit qualities would converge and ultimately would be guaranteed by the single monetary union. The chart below shows Italian 10-year Treasury yields.

After falling in the late-1990s into the creation of the Eurozone on January 1, 2000, yields remained stable and low until the Eurozone crisis in 2009 when it became clear that not all credits were created equal within the Eurozone. However, the subsequent easy monetary policy by the European Central Bank (ECB) as well as the effects of the central bank’s asset-purchase program lowered yields to historically low levels.

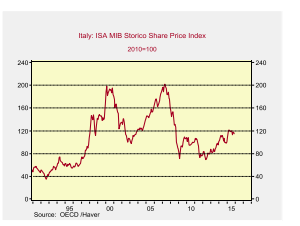

The chart below shows the Italian stock index over the same time period. Stocks have experienced greater volatility as the underlying economic growth has remained constrained.

Following the Eurozone crisis, Italian banks avoided an EU-backed bail-out.

However, as a result, the country’s banks hold a disproportionate level of NPLs, especially when compared to banks in countries that were able to remove NPLs from their balance sheets through a bail-out (e.g., Spain, Ireland).

Scale Bank Rescue

In November 2015, the Italian government restructured four small banks. Implemented ahead of the new Eurozone “bail-in” directive, the restructuring pushed losses onto not only stock and bond holders but also absorbed deposit accounts that were larger than €100,000 before using government funds. The bank rescue was relatively small at €250 mn, but it gathered public attention after a pensioner committed suicide as a result of losing his life’s savings in the restructuring. It appears that he owned the bank’s bonds, believing them to be low-risk assets. A complicating twist to the Italian bank situation is that the banks often sold their subordinated bonds to retail investors as a substitute for deposits, and depositors mistook them for safe

investments. As a result, many Italian retail investors are overexposed to the banking system bonds. Consequently, the Italian government has initiated a case-by-case resolution to help “irregular bond purchasers” who bought the bonds without understanding the risks involved. This policy is likely to fail due to the difficulty in applying for it in practice, the increasing popular opinion demanding a “blanket” guarantee to retail clients and the EU opposition to guarantees.

Bad Bank

Italy has not been able to create a “bad bank” where it could accumulate the nonperforming loans. Spain and Ireland were able to help their banking systems by creating bad banks during the 2011-2012 bail-out crises. However, Italy has encountered recent opposition from the EU as the creditor nations are now more reluctant to bail out other countries’ banks. During the 2011-2012 Eurozone crisis, the monetary union was more open to providing support for countries that officially sought a bail-out, while current regulations oppose the use of “state aid” to bail out private banks. The use of EU funds to bail out banks has been virtually eliminated under the new BRRD rules. Additionally, under the new rules, each large depositor is liable for knowing the underlying health of the bank. In reality, it will be hard for retail investors to know this so it would mean that depositors should diversify their risks by opening several smaller accounts in various banks or move their money across the borders to other European countries. For example, neighboring Spanish banks were restructured via Eurozone bail-outs in 2012, thus reducing bad debts and currently

leaving them in a healthier financial position than Italian banks. In this banking environment, the possibility of bank runs will be increased as depositors grow increasingly nervous about the safety of their savings. Similar to the U.S. bank runs of 1907, rumors can feed panic, which can lead to bank runs that ruin even healthy banks. In addition, if a bank is forced to liquidate a loan under stress, the price discount it would have to accept would in turn weaken the bank’s financial health, leading to more deposit withdrawals and creating a never-ending vicious cycle. A deposit insurance system usually soothes some retail investors’ worries over bank runs.

Although no EU-wide deposit insurance is in place, an Italian deposit insurance system does exist (Interbank Deposit Protection Fund), which should protect deposits of up to €100,000. According to estimates, the average size of a bank account in Italy is €13,200 (source: MutuiOnline), so it appears that many bank accounts would be protected by the insurance. However, the size of actual funds available for deposit insurance is uncertain as the latest data is from 2013. The larger banks will also require significantly larger funds. For example, Monte dei Paschi, Italy’s third largest bank, holds roughly €45 bn of NPL. By comparison, the private losses in the restructuring of the four small banks in November were about €790 mn.

Positive Developments

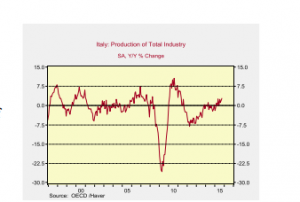

There are a couple of positive developments in Italian banking. First, in November, the rating service Fitch raised its outlook for Italian banks to stable from negative. Although ratings agencies are not always right, this should at least allow Italian banks to borrow at more attractive rates. Second, loan creation growth has continued. Increasing loans potentially means more diversification away from the nonperforming loans. Of course, this trend would only be helpful if the new loans are of higher quality, resulting in less nonperforming loans, and the new loans are not simply used to refinance the nonperforming loans. Third, a wave of consolidation in the Italian banking sector may mean that some of the weaker and smaller banks would be absorbed by safer counterparties. However, we note that in the long run this may bring its own problems and bigger does not necessarily mean safer in the current Italian banking landscape. Last, but not least, the Italian economy is forecast to grow at a slow but steady rate this year. The chart below shows the country’s year-over-year GDP growth

Perhaps more importantly, Italy is finally seeing a positive rate of industrial production growth, although production has not surpassed its pre-2008 high. Some of this industrial growth could be due to the low petroleum product prices, so we may see a slight pullback of industrial growth when crude prices rebound.

Italy’s Banking Crisis – The Way Forward

The Italian banks’ current situation is made more difficult by the political wrangling both within the country and the EU. Although the Italian government supports a wide-scale banking system restructuring, EU opinion has swung to opposition. The Eurozone’s monetary policy is currently largely driven by Germany, which is trying to avoid using its taxpayers’ money to bail out other countries’ bank bond and deposit holders. During the Cyprus banking crisis, the Eurozone took a tougher stance for the first time, forcing private bond and deposit holders to suffer losses. Germany has to balance two conflicting goals. On the one hand, it does not want to use its own funding to guarantee other Eurozone countries’ depositors. German public opinion especially opposes covering other countries’ bad debts while the German people have accepted austerity.

On the other hand, it does not want leaving the Eurozone to become an attractive alternative. Thus, it has to give Italy just enough to keep it from leaving the monetary union. We do not anticipate a solution to emerge soon. The two sides will likely come to a workable solution, but only after an extended period of brinkmanship. The most likely outcome would be that the EU and Italy agree to a solution that falls within the “direct state aid” category, despite northern European opposition. It is clear that Italy needs some sort of a solution to help clear the bad loans out of the banking system and prevent bank runs. With almost one-fifth of the country’s loans deemed nonperforming, the loan problem needs to be addressed and will not simply “work itself out.” Italy is arguing for access to EU funding to clear the bad debts, while the EU is trying to push haircuts on private investors and depositors. In the longer term, a possible EU solution could involve a loan to Italy to boost its deposit insurance funds. However, we do not expect a solution to be reached until the banking situation has deteriorated further.

Ramifications The uncertainty in the Italian banking sector is likely to increase volatility for the banking sectors of weaker Eurozone countries. We could also see increased cross-border capital flows as depositors will likely move money to a country with a more favorable banking system. If countries implement capital restrictions as a result of the capital outflows, bigger Eurozone-wide problems could develop. Although other countries’ banking sectors could be affected in the short term, contagion risk to other countries is still low.

Emerging market currency rout is likely to accelerate "import" deflation.

Falling commodity prices will only compound the deflationary environment.

Increased deflationary pressures will delay rate hikes from the BoE.

BoE likely to be one of the first to conduct balance sheet expansion should deflationary pressures continue.

As part of our broader view of a global slowdown developing in the second half of 2015 and into 2016 due to weakness in Emerging Markets, we see potential for a severe correction in sterling developing in the months ahead. Coming off the mid-April lows, the pound has been trading in a tight range of 1.5150-1.5650, proving to be one of the more resilient currencies against the US dollar year to date. Given the turbulent economic picture globally, we see considerable risks to sterling going forward, and would be looking to short the pound with a 6 to 9 month price target of 1.40 to 1.35, which would result in new multi-year lows.

Emerging market currency rout is likely to accelerate "import" deflation

The ongoing rout in commodity prices and emerging market currencies is likely to accelerate "import" deflation within the United Kingdom, a trend we should start seeing to develop in the ONS inflation figures going into the second half of 2015. Sterling has strengthened considerably against some of its key trading partners throughout July, most notably against the South Korean won in the emerging world and the euro in more developed circles. Sterling has gained 10% against the won this year alone, 12% against the euro and a staggering 21% against the Aussie dollar. It will be the rapid deterioration against key export currencies like the won however that will have the BoE most concerned. Perhaps even more ominous is the fact that sterling is still actually weaker by 2% against the yuan in 2015 despite the recent devaluations, highlighting just how much further China could devalue the yuan to regain a competitive footing with its export dependent neighbors. Any severe appreciation against the yuan going forward is sure to provoke some sort of retaliatory response from the BoE.

Falling commodity prices only compound the deflationary environment

The UK has already been contending with deflationary pressures since the -0.1 percent decline recorded in May - the first official deflation reading in over 50 years. Subsequent CPI readings in June, July and August have been anemic at best. An appreciating currency will only add to these pressures, especially given the broad fall in commodity prices over the same period. Despite sterling weakening nearly 6% against the dollar year to date, the fall in inflation-related commodities such as crude oil has been much sharper, hovering near a 6-year low and producing a net deflationary effect for the UK. Again this trend is likely to cement itself going forward into 2015 and will be one of the key driving force behind our short GBP/USD thesis.

Increased deflationary pressures will delay rate hikes from the BoE

We believe the market will continue to abandon the notion that the BoE will raise rates once the extent of the deflationary threat confronting global markets is fully digested. Rate hike expectations have been one of the key pillars of support for sterling in 2015, setting up the stage for a significant reversal in the pound should these expectations begin to fade.

Since the deflationary print in May, the mild sell-off in sterling already suggests a portion of the market is leaning in this direction.

BoE likely to be one of the first to conduct balance sheet expansion should deflationary pressures continue

Looking through the next 6 to 9 months, one of the biggest events we see on the horizon is a return in some shape or form of significant balance sheet expansion or increased jawboning/direct currency intervention by one or more of the developed world's central banks,. The growing threat of deflation worldwide is likely to spark at least one major player into action, and we would not be surprised if the BoE came to the forefront in this regard.

Summary

We are calling for a drop in GBP/USD, with our first target to breakthrough multi-year lows to 1.40 before settling at 1.35 in the next six to nine months. We see a deteriorating deflation picture in the UK, revised rate hike expectations, combined with risk-off sentiment in global financial markets to be the key driving forces behind the move.

Our data now shows a remarkable 70 percent of open GBP/USD positions in our sample are long; a contrarian view leaves us firmly bearish. The only caveat is straightforward—retail positions are often at their most one-sided at major market turns. And indeed, our Speculative Sentiment Index shows the largest ‘crowd’ long position since the GBP/USD reversed higher off of $1.41 mark just one month ago.

Such extremes are only clear in hindsight, however; until we see concrete signs of a sentiment shift we will remain in favor of selling into GBP/USD weakness.

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.

Learn forex trading with a free practice account and trading charts from FXCM.

My friends who are gold bugs need to wake up and realize the overvaluations of this commodity which, quite frankly has no idustrial value. Gold is in huge supply, with like no demand. Besides using gold for our rockets and our new telescopes , which will enable us, to un shade the dark areas in space, there's nothing else gold has industrial use for. You see gold and silver are found underground mother earth In deep crevaces with streams of water. Now considering gold and silver basically grow naturally together in these crevaces the botton line the silver from these crevaces has already been mined. There is not much mineable silver left on mother earth to meet demand. You see, we actually need silver for our technology and so the funny thing is when you understand the cost versus profit margin, the startup costs alone far exceed any type of benefit. There already is an overwhelming amount of gold miners that are on the verge of bankruptcy. Miners are missing interest payments on the colaterlized loans they took out in the first place, what we see Is when you examine the spot gold price, you'll start to see trends where the spot gold price will fall below 1200 dollars an ounce, you'll see It fall to 1150 and then what happens is, you see indsiders whom have an interest in these minging companies step in and prop up this gold price back to 1200 an ounce. 1200 is the tetering figure, at tuat price miners can barely pay their debts but it enables them to avoid filing bankruptcy. So in the long term my price target for an ounce of gold is somewhere in the $700 to $500 dollar mark Oover the next 5 to 7 years. The best advice I can give you is if you have an gold bullion in your safe, or gold jewlery I suggest you sell now for a profit. You know you can always make money betting on the downside, remember my friends the old gold standard back in it's hayday in the 18th century, the old standard lasted a total of only 65 months and their were 3 great recessions during that time period. People need to understand that the private sector is completely transparet, so what that means is you can always learn how to discern economic ebs and flows. Our best banks like Morgan Stanley, J.P. Morgan, Citi bank, Merrill Lynch and Raymond James, and of course Goldman Sax, have the accurate data and realize this, our Bankd and Bankers are not the enemy, you can jump on a site like investorwand.com where these banks have their analysts publically annoince their stock picks, abd so forth, I mean Goldman Sax is such an amazing bank because they have the most educated scholars who went to Yale on a fullride. The minute you try to make an excuse and blame bakers or corporations for why your life sucks, the minute A guy like me will tell you, it's not Capitalism or the private sector to with whom you should be made at, what you should be mad at is crony over reaching govnment. And do you want to know why I say that, well that's becuz my friends crony gov't is not transperent. How can you be mad at millionairer or billionaire bakers for being filthy rich, they provide you with free information that is all public information, for you to go learn and become informed on how to be properly invest your savings. Listern the first thing ypu do is takre your money out of your bank account and call scottrade or TD ameritrade and open a brokerage account. It's just like a bank account, you can keep your money in cash, and occasionally for example when you do your homework and take advice from Goldman sax's best analyst Heather Billini, 6 months ago Heather recommended a buy signal on Facebook, ticker symbol FB on nasdaq, when it was $50 dollars a share, you could have put

your money in and could have.made a substantial profit with the appreciation of Facebook's capital gains , have you looked yet at Facebook's stock price, it's now trading approx $106 dollars a share, and my target is $500 in 3 years, no kidding, take the time to read through public information, the private sector has to be transparent there's quaterly audits and rules and regulations set by the SEC AND FINRA, that companies have to follow, the system in America is simply quite unique. The more times you point the finger at some one else for why the reason your poor, the minute you need to take a step back and look in the mirror, the only fault for why your life sucks , is simply put, your either too lazy, or just an idiot. So all I can say is I was a stock broker for a year on wall street back in.2010, I've been around millionaire and spoken to billionares, and SIMPLY put the reason why they are rich is because while your working your little 9 to 5 job where you probably don't even work, because let's face it, most of you are clock watchers who avoid doing work while your at your so called job, My friends here's a news flash , your a lazy piece of shit and your weak. At the end of the day while you run home to your DVR and watch your stupid sitcoms, and then while your dumbass is sleeping at nite, millionare in the banking industry are working, and they never stop working, at their job, they are engaged, nuff said. the global economy is always open, let this be a wake up call, your time is running out. Sell your gold, lmao idiots all of you.

As we maintain our view of rising U.S. rates and hence lower gold prices with a three-month target of $1,100 an ounce and 12-month target of $1,000 an ounce, we are recommending shorting gold.

True to being a spy, not much is known about Sir William Davidson. On paper, he was listed as the 1st Baronet of Curriehill, and records also show that he was a Scottish tradesman based out of Amsterdam. Underneath all that is a man who served as a spy for the King.

Davidson first appears on record in Holland during 1640, but not much is known about where he came from or who his descendants were. He was a trader, dealing throughout the Baltic reason, he was married and he’d stated he was 29 years old. His wife died after 12 years of marriage, and he remarried but his new wife died 6 years later. By then the English Civil War was erupting and Davidson had chosen the Stuarts who supported Charles II.

He was an ardent supporter of Charles, and used his financial means to help put the monarchy back into power. He also supplied the exiled Charles actively, part of network supporting him as the conflict was settled. When Cromwell died, the monarchy got its restoration and Charles returned to power. The transition was swift, in part thanks to information Davidson had obtained through his dealings as a trader. His travels had taken him all through Amsterdam and Stockholm, and he’d had plenty of time to gather information from the merchant’s he’d met along the way. Word travelled well outside of England, it seemed.

Charles made him conservator of the staple in Veere for his loyalty. His life after 1666 is a little muddled. He was known to have traded tobacco in Virginia in 1672, and believed to have settled in Scotland around the year 1678. He died sometime near 1689, and possible in Edinburgh, but Davidson very much vanished back into the merchant trade. Perhaps a glimpse of just how important a role merchants played throughout history.

One of the driving factors in the creation of our national currency was the National Bank Act of 1864. The legislation is actually composed of two acts, and they established several important precedents for our current financial system. The two acts dissolved the idea of a state bank issued currency, which ultimately helped early entrepreneurs conduct business between states.

The initial act was part of President Lincoln’s broader plan to fund the federal government throughout the Civil War. Lincoln used his money to finance the war against the Confederacy through the purchase of federal bonds and state bank issued currency of the time. This initial attempt failed, giving way to the true National Bank Act of 1864.

The rule created so-called “Greenbacks” and established the notes as the nation’s currency. The act also created a new Office of the Comptroller of the Currency, which was a part of the Department of Treasury.

The First National Bank of Philadelphia was the first bank to apply for a charter under the new legislation, but it was not the first bank to operate under the new rules. That honor goes to The First National Bank of Davenport.

In order to finalize the state bank issued notes, a subsequent act was passed in 1865. This legislation made it possible to tax notes from state banks starting in 1866. This forced all non-federal currency from common circulation, and created a new demand for deposit accounts.

I think we are at the tag end of the recent unbelievable bout of yen strength.

Triggered by the Bank of Japan’s shocking move to negative interest rates (NIRP), it has been driven by a massive unwind of hedge fund positions in everything around the world that were all financed by short yen positions.

The memo is out now, and the bulk of the “hot money” positions are gone. After some fits and starts, I expect the yen to resume its long-term structural downtrend shortly.

If for any reasons you can’t do options, just buy the ProShares Ultra Short Yen ETF (YCS) outright. This is the best entry point in a year.

“Oh, how I despise the yen, let me count the ways.”

I’m sure Shakespeare would have come up with a line of iambic pentameter similar to this if he were a foreign exchange trader. I firmly believe that a short position in the yen should be at the core of any hedged portfolio for the next decade.

To remind you why you hate the currency of the land of the rising sun, I’ll refresh your memory with this short list:

1) With the world’s structurally weakest major economy, Japan is certain to be the last country to raise interest rates. Interest rate differentials between countries are the single greatest driver of foreign exchange rates. That means the yen is taking the downtown express.

2) This is inciting big hedge funds to borrow yen and sell it to finance longs in every other corner of the financial markets. So “RISK ON” means more yen selling, a lot.

3) Japan has the world’s worst demographic outlook that assures its problems will only get worse. They’re just not making enough Japanese any more. Countries that are not minting new consumers in large numbers tend to have poor economies and weak currencies.

4) The sovereign debt crisis in Europe is prompting investors to scan the horizon for the next troubled country. With gross debt well over a nosebleed 270% of GDP, or 160% when you net out inter agency cross holdings, Japan is at the top of the list.

5) The Japanese ten-year bond market, with a yield AT AN ABSOLUTELY EYE-POPPING -0.08%, is a disaster waiting to happen. It makes US Treasury bonds look generous by comparison at 1.70%. No yield support here whatsoever.

6) You have two willing co-conspirators in this trade, the Ministry of Finance and the Bank of Japan, who will move Mount Fuji if they must to get the yen down and bail out the country’s beleaguered exporters and revive the economy.

When the big turn inevitably comes, we’re going from the current ¥112.75 to ¥125, then ¥130, then ¥150. That works out to a price of $150 for the (YCS), which last traded at $76.88. But it might take a few years to get there.

If you think this is extreme, let me remind you that when I first went to Japan in the early seventies, the yen was trading at ¥305, and had just been revalued from the Peace Treaty Dodge line rate of ¥360.

To me the ¥112.75 I see on my screen today is unbelievably expensive.